IRS Form 5472 Guide for Foreign-Owned LLCs | 2026 Deadlines, Penalties

- Arik Rozen (CPA, MBA)

- Jun 19

- 25 min read

Updated: Jun 21

In This Guide:

→ What Is IRS Form 5472?

→ Who Needs to File Form 5472?

→ What Triggers the Filing Requirement?

→ The Zero-Income Trap

→ Form 5472 Deadlines for 2026

→ How to File Form 5472 — Step by Step

→ Penalties for Not Filing

→ How to Fix a Missed Deadline

→ Common Mistakes to Avoid

→ Frequently Asked Questions

IRS Form 5472 is one of the most misunderstood — and most penalized — tax forms in the United States. If you are a non-U.S. resident who owns a U.S. LLC or corporation, this form was created specifically for you. And the IRS takes it very seriously: failing to file carries an automatic penalty of $25,000 per form, per year — even if your business made absolutely no money.

In 2020 alone, the IRS processed over 80,000 Form 5472 filings. Tens of thousands more went unfiled — most by founders who simply didn't know the requirement existed.

This guide covers everything you need to know: who must file, what triggers the requirement, when it's due, how to file it correctly, and what to do if you've already missed the deadline.

What Is IRS Form 5472?

Form 5472 is an information return filed with the IRS by foreign-owned U.S. corporations and certain foreign corporations engaged in U.S. business. Its official IRS name is "Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business."

Despite that long official title, the form has one simple purpose: to tell the IRS who owns your U.S. company and what financial transactions occurred between you and that company.

It is not a tax payment form. You do not owe money when you file it. It is a transparency and disclosure requirement — and the IRS enforces it with automatic penalties that have no maximum cap.

Form 5472 vs. Form 5471 — What Is the Difference?

These two forms are frequently confused, and for good reason — they sound nearly identical. Here is the key difference:

Form | Who Files It | What It Reports |

Form 5472 | Foreign-owned U.S. companies | Transactions between a U.S. entity and its foreign owner |

Form 5471 | U.S. persons who own foreign corporations | Ownership and financial data of a foreign company |

The simplest way to remember it: if you are a foreigner who owns a U.S. company, you deal with Form 5472. If you are an American who owns a foreign company, that is Form 5471. Different direction of ownership, different form.

💼 Arik's Corner"In 22 years of filing these forms, I have never once had a client say 'I'm glad I didn't file Form 5472.' I have had many say the other thing."— Arik Rozen, CPA

Who Needs to File Form 5472?

Not every U.S. business owner needs to file Form 5472 — but if you are a non-U.S. resident, the chances are high that you do. There are four main categories of entities required to file.

1. Foreign-Owned Single-Member LLCs — The Most Common Case

This is the scenario that affects the vast majority of international founders.

If you are a non-U.S. resident who owns 100% of a U.S. single-member LLC, your company is classified by the IRS as a "disregarded entity." This means the LLC is invisible for federal income tax purposes — but it is not invisible for Form 5472 purposes.

You must file Form 5472 attached to a pro forma Form 1120 — a corporate return that exists solely to carry the Form 5472 attachment. You do not file a standalone Form 5472. The two forms travel together as a package.

This catches thousands of founders off guard every year, because their LLC formation service, their bank, or their registered agent never mentioned it.

2. Foreign-Owned U.S. C-Corporations

Any U.S. C-Corporation where a foreign person owns 25% or more of the stock at any point during the tax year must file Form 5472.

Note the threshold: 25%, not 50%, not majority control. A minority foreign shareholder can trigger the filing requirement for the entire corporation.

Example: A Delaware C-Corp with two founders — one U.S. citizen owning 80% and one German citizen owning 20% — does NOT trigger Form 5472 because the foreign ownership is below 25%. Change that split to 75%/25% and the filing requirement activates immediately.

3. Foreign Corporations Engaged in U.S. Business

A foreign corporation that conducts trade or business within the United States and has reportable transactions with related parties must also file Form 5472.

Example: A German GmbH with a branch office in New York that pays management fees to its German parent company would need to file Form 5472 to report those payments.

4. Multi-Member LLCs — Do They File Form 5472?

Generally, no — but they have their own separate filing requirements.

If your LLC has two or more foreign owners and is taxed as a partnership, you do not file Form 5472. Instead, you file Form 1065 (U.S. Return of Partnership Income) along with Schedules K-1, K-2, and K-3. The deadline is different, the penalties are different, and the forms are completely different. Do not confuse the two.

Quick Reference — Who Files What?

Entity Type | Foreign Ownership | Required Forms | Deadline |

Single-Member LLC | 100% foreign-owned | Form 5472 + Pro Forma 1120 | April 15 |

C-Corporation | 25%+ foreign-owned | Form 5472 + Form 1120 | April 15 |

Multi-Member LLC | Foreign partners | Form 1065 + K-1 / K-2 / K-3 | March 15 |

Foreign Corporation | Operating in U.S. | Form 5472 | April 15 |

💼 Arik's Corner: "The number one question I get from new clients: 'I have a single-member LLC — do I really need to file a corporate tax return?' Yes. It is called a pro forma Form 1120. It sounds ridiculous. It is completely real. File it."— Arik Rozen, CPA

What Triggers the Form 5472 Filing Requirement?

Knowing you need to file Form 5472 is step one. Knowing what actually triggers the requirement is step two — and this is where most international founders get tripped up.

The filing requirement is activated by what the IRS calls a "reportable transaction." If a reportable transaction occurred during the tax year between your U.S. company and a related foreign party, the form must be filed.

What Is a Reportable Transaction?

A reportable transaction is any transfer of money or property — or the right to use property or services — between your U.S. entity and a related foreign party. This includes:

Sales of inventory, goods, or products

Purchases of equipment, software, or assets

Royalty payments for intellectual property or licenses

Interest payments on loans

Rent payments for real or personal property

Compensation for services rendered

Capital contributions from the foreign owner to the U.S. company

Distributions from the U.S. company back to the foreign owner

Company formation and setup costs paid by the foreign owner

What Is a "Related Party" Under IRS Rules?

For Form 5472 purposes, a related party includes:

Any direct or indirect foreign shareholder who owns 25% or more of the reporting corporation

Any person related to the reporting corporation or to a 25% foreign shareholder

Certain foreign corporations engaged in U.S. trade or business

In plain terms: if you own the U.S. company and you paid anything into it or took anything out of it, that is a reportable transaction between you (the related foreign party) and your company.

Real-World Examples of Reportable Transactions

Here are the most common situations we see:

You wired $5,000 from your personal foreign bank account into your U.S. LLC bank account to cover operating costs. That is a capital contribution — reportable transaction.

You paid your state's annual registered agent fee ($50–$150) using your personal funds. That is a formation/maintenance cost — reportable transaction.

Your U.S. LLC paid you a distribution of $3,000. That is an owner distribution — reportable transaction.

Your U.S. company paid a $500,000 royalty to your overseas parent company for using patented technology. Reportable transaction.

Your foreign parent loaned your U.S. company $10,000 at 5% annual interest. Both the loan principal and each interest payment are reportable transactions.

⚠️ Important Even non-monetary transactions must be reported. If your foreign parent company provided free marketing services, free use of intellectual property, or any other benefit without payment, that is still a reportable transaction and must be disclosed on Form 5472.

The Zero-Income Trap: Why "No Revenue" Does Not Mean No Filing

This is the single most costly misunderstanding among international founders, and it is the reason our team handles thousands of late-filing penalty cases every year.

The IRS does not base the Form 5472 filing requirement on whether your business made money. It bases it on ownership structure and the occurrence of reportable transactions.

So if your U.S. LLC generated exactly $0 in revenue — no clients, no sales, no income of any kind — you may still be required to file Form 5472.

Why Almost No LLC Is Truly "Dormant"

For your U.S. LLC to have zero reportable transactions, none of the following can have occurred during the entire tax year:

You formed the company during the year (formation fees = reportable transaction)

You paid your registered agent's annual fee (maintenance cost = reportable transaction)

You opened or maintained a U.S. bank account with your funds

You transferred any money into or out of the company

You used the company's address, EIN, or legal status for any purpose

You paid any subscription, software, or tool under the company's name

In practice, a truly dormant LLC with zero reportable transactions is extremely rare. If you did any single one of the above — even paying a $50 registered agent fee from your personal account — a reportable transaction occurred, and you are required to file.

💼 Arik's Corner: "Your LLC made $0 this year. Congratulations — you may still have to file. The IRS does not grade on a curve."— Arik Rozen, CPA

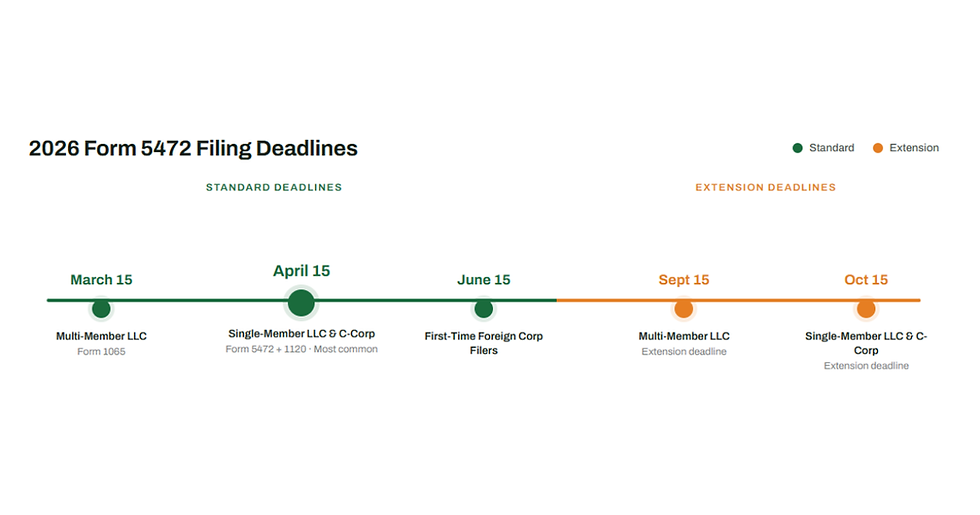

Form 5472 Filing Deadlines for 2026

The deadline for Form 5472 depends entirely on your entity type. Missing it — even by one day — triggers an automatic $25,000 IRS penalty. There are no grace periods and no warnings before the penalty is assessed.

Standard Deadlines by Entity Type

Entity Type | Standard Deadline | With Extension | Extension Form |

Single-Member LLC (Foreign-Owned) | April 15, 2026 | October 15, 2026 | Form 7004 |

C-Corporation (Foreign-Owned) | April 15, 2026 | October 15, 2026 | Form 7004 |

Multi-Member LLC (Partnership) | March 15, 2026 | September 15, 2026 | Form 7004 |

Foreign Corporation (U.S. Business) | April 15, 2026 | October 15, 2026 | Form 7004 |

First-Time Foreign Corporation Filer | June 15, 2026 | N/A | N/A |

Important Notes on Extensions

Filing an extension via Form 7004 extends the deadline to file your return — it does not extend the deadline to pay any taxes owed. For most foreign-owned LLCs with no U.S. income tax liability, this distinction doesn't matter. But it is worth knowing.

Also: an extension must be filed before the original deadline. You cannot file Form 7004 after April 15th and retroactively extend your deadline.

Weekend and Holiday Adjustments

When a filing deadline falls on a Saturday, Sunday, or federal holiday, it automatically shifts to the next business day. Always verify the exact date for the current tax year, as this changes annually.

💼 Arik's Corner: "April 15th is not a suggestion. It is not a guideline. It is not 'around springtime.' It is April 15th."— Arik Rozen, CPA

How to File IRS Form 5472 — Step by Step

Filing Form 5472 involves more than filling in a single form. Here is the complete process, exactly as our CPA team executes it for every client.

Step 1 — Determine Your Entity Classification

Before anything else, confirm which entity type you are filing for. This determines which forms you need, which deadlines apply, and how the Form 5472 is attached and submitted. Refer to the entity comparison table above if you are unsure.

Step 2 — Obtain Your EIN

Your U.S. company must have an Employer Identification Number (EIN) before you can file. If you do not yet have one, you must apply for it via IRS Form SS-4. Without an EIN, the IRS cannot process your return.

Step 3 — Identify and Categorize All Reportable Transactions

Gather your records for the full tax year and identify every transaction between your U.S. entity and any related foreign party. Categorize each one:

Monetary transactions: cash transfers, payments, loans, interest, royalties, rents

Nonmonetary transactions: use of property, services provided without cash payment

Less-than-full-consideration transactions: anything provided below market value

Convert all foreign currency amounts to U.S. dollars using consistent IRS-approved exchange rates.

Step 4 — Complete Form 5472 Section by Section

Form 5472 has five main sections:

Section 1 — Reporting Corporation: Your company's name, EIN, address, tax year, and number of Forms 5472 being filed.

Section 2 — 25% Foreign Shareholder Information: Name, address, country of organization, and ownership percentage of the foreign owner.

Section 3 — Related Party Information: Details of the related party involved in the reported transactions.

Section 4 — Monetary Transactions: All cash-based transactions with the related party, reported in U.S. dollars by category (sales, rents, royalties, interest, etc.).

Section 5 — Nonmonetary and Less-Than-Full Consideration Transactions: Description and estimated value of any non-cash transactions.

Step 5 — Attach to Pro Forma Form 1120 (for Single-Member LLCs)

If you are a foreign-owned single-member LLC, Form 5472 cannot be submitted alone. It must be attached to a pro forma Form 1120 — a version of the corporate tax return prepared specifically to serve as the carrier document. The pro forma 1120 is not a full corporate return; it exists only to give Form 5472 a vehicle for submission.

This step is where DIY filers most commonly make errors. The pro forma 1120 must be prepared correctly or the entire filing can be rejected.

Step 6 — File via IRS Authorized E-File Provider

Completed filings must be transmitted to the IRS through an authorized electronic channel, or submitted via certified mail to the correct IRS address. E-filing through an IRS Authorized e-File Provider (like form5472.online) is the fastest and most secure method, and provides a filing confirmation upon receipt.

Step 7 — Retain Your Filing Confirmation and Records

Once filed, retain a complete copy of the submitted forms and all supporting transaction records. The IRS recommends keeping these records for at least seven years. Because the statute of limitations remains open indefinitely for unfiled Form 5472s, strong record-keeping is your long-term protection.

🗂️ Skip the complexity. Our licensed CPA team handles every step above — from entity classification to IRS submission — with a Zero Penalty Guarantee.

Field-by-Field Walkthrough: Every Section of Form 5472 Explained

The steps above outline the filing process. This section goes deeper — walking through every field on the actual form in the exact order they appear, with examples and common errors for each one.

Preparing the Pro Forma Form 1120 (The Cover Sheet)

Form 5472 cannot be filed on its own. The IRS requires it to be attached to a pro forma Form 1120 — a simplified corporate tax return that serves purely as a carrier document. You will not report income, expenses, or taxes on this form. You only fill in a handful of identification fields.

Line 1a — Corporation name: Enter the exact legal name of your LLC as registered with the IRS. This must match your EIN letter character for character. Even "LLC" versus "L.L.C." can cause processing issues.

Line 1b — EIN: Your 9-digit Employer Identification Number in the format XX-XXXXXXX.

Line 2a — Principal business activity: A brief one-line description such as "E-commerce retail" or "Software consulting."

Address block: Use your registered agent's address if you do not have a U.S. business address.

Top of form: Write "Foreign-Owned U.S. DE" in large text across the very top of the first page. The IRS requires this label to identify the return as a disregarded entity filing. This is not optional.

Leave ALL income lines blank. Leave ALL deduction lines blank. Leave ALL tax computation lines blank. Do not enter zeros — leave them completely empty.

💼 Arik's Corner"The pro forma 1120 is probably the strangest form in the entire IRS system. You fill in your name and address, write 'Foreign-Owned U.S. DE' across the top, leave everything else blank, and submit it as a corporate tax return. I have been doing this for 22 years and it still feels absurd. But it is what the IRS requires."— Arik Rozen, CPA

Form 5472 Page 1 — Header and Tax Year

The top of page 1 establishes the identity of your filing entity and the tax year being reported. Errors on the header section are the number one cause of IRS rejection.

Entity type checkbox: Check "Foreign-owned domestic disregarded entity" if you are a foreign-owned single-member LLC. C-Corporations check the other box.

Line 1a — Name of reporting corporation: Your LLC's legal name, exactly matching your EIN letter.

Line 1b — EIN: Same number as on the pro forma Form 1120.

Line 1c — Total assets: The total assets of the LLC at year-end. This is balance sheet value, not revenue. If the LLC had no assets, enter 0.

Line 1d — Principal business activity code: Your 6-digit NAICS code (example: 454110 for e-commerce, 541511 for software development).

Line 1e — Country of incorporation: United States.

Tax year begin and end dates: For calendar year filers, enter 01/01/2025 and 12/31/2025. These dates must match the pro forma Form 1120. If your LLC was formed mid-year, the begin date is the formation date, not January 1.

Part I — Foreign Owner Information

Part I identifies you — the foreign person or entity that owns the U.S. LLC. This is the most mistake-prone section for foreign owners.

Line 2a — Name of foreign related party: Your full legal name as an individual, or the legal entity name if a foreign company owns the LLC.

Line 2b — U.S. taxpayer identification number: Most foreign individuals do not have a U.S. SSN or ITIN. Leave blank if you do not have one.

Line 2c — Foreign taxpayer identification number (FTIN): Your tax ID number in your home country. UK owners enter their UTR. Israeli owners enter their 9-digit national ID. German owners enter their Steuer-ID. This field is required if you have a foreign tax ID.

Line 2d — Reference ID number: Only needed if you do not have an FTIN. You can create a consistent reference code such as "OWNER-001."

Line 2e — Address: Your full foreign residential or business address. Do not use a U.S. address here.

Line 2f — Country of organization or citizenship: The country where you are a tax resident or where the foreign entity is incorporated.

Line 2g — Principal countries where business is conducted: Where you primarily operate. Usually the same as Line 2f.

Important: Leaving the FTIN blank when you have one is a common audit trigger. The IRS has been strict about this since 2018. If you genuinely do not have a foreign tax ID, enter "NONE" and attach a brief written explanation.

Part II — U.S. Reporting Corporation

Part II describes the LLC itself. This section is usually straightforward.

Line 3 — Principal business activity: One sentence describing what the LLC does. Examples: "E-commerce retail sales" or "Software development consulting."

Line 4a — Percent ownership by foreign related party: For a single foreign owner, enter 100.

Line 4b — Percent of voting stock owned: Usually the same as Line 4a. Enter 100.

Line 5 — Is the reporting corporation a member of an affiliated group: Check No. Most single-member LLCs are not part of an affiliated corporate group.

Part III — Related Party Relationships

Part III declares the legal relationship category between you and the LLC. Check every box that applies.

Line 6a — Foreign person owns 25% or more of the reporting corporation: Check this box. You own 100%.

Line 6b — Foreign related party and reporting corporation are related: Check this box. You control the LLC.

Lines 7 through 11 — Nature of relationship: For a standard single-member LLC owned by a foreign individual, check "individual" on Line 7.

Most filers only need to check one or two boxes in this entire section.

💼 Arik's Corner"Part III is four checkboxes. Part II is four fields, two of which are just the number 100. If you are spending more than five minutes on these two sections combined, something has gone wrong."— Arik Rozen, CPA

Part IV — Monetary Transactions (The Most Critical Section)

Part IV is the heart of Form 5472. Report every dollar that moved between the LLC and you during the tax year. Enter the total amount for the entire year on each line — not transaction by transaction.

Line 12 — Sales of inventory: Total value of goods the LLC sold that were purchased from you.

Line 13 — Purchases of inventory: Total value of goods the LLC bought from you to resell.

Line 14 — Sales of property other than inventory: Property the LLC sold to you.

Line 15 — Purchases of property other than inventory: Property the LLC purchased from you.

Line 16 — Rents paid: Rent the LLC paid to you for any property.

Line 17 — Rents received: Rent you paid to the LLC.

Line 18 — Royalties paid: License fees or intellectual property payments the LLC made to you.

Line 19 — Royalties received: Royalty payments you made to the LLC.

Line 20 — Insurance premiums: Rare for most small LLCs.

Line 21 — Interest paid: Interest the LLC paid you on a loan.

Line 22 — Interest received: Interest the LLC received on a loan to you.

Line 23 — Compensation paid for services: Total payments the LLC made to you for consulting, management, or other services. This is one of the most commonly used lines.

Line 24 — Compensation received for services: Payments you made to the LLC for services.

Line 25a — Amounts borrowed from owner: Money you transferred into the LLC, including formation costs, registered agent fees, and operating expenses paid from your personal funds. The IRS treats all owner-paid costs as capital contributions reported on this line.

Line 25b — Amounts loaned to owner: Money the LLC lent back to you. Uncommon.

Line 26 — Other amounts paid: Catch-all for anything not listed above. Attach a written description explaining the payment.

Line 27 — Other amounts received: Other receipts not covered above.

Real-world example: A UK-based founder owns a Delaware LLC providing consulting services. During the year, they transferred $15,000 from their personal UK bank account into the LLC to fund operations, and the LLC paid them $2,400 for consulting work. They also paid the $149 registered agent renewal from personal funds. The filing would show Line 25a as $15,149, Line 23 as $2,400, and every other line as $0.

Three rules for Part IV that prevent penalties:

First — do not leave any line blank. A blank field is not the same as $0 in the IRS processing system. Enter zero on every line where no transaction occurred.

Second — do not use estimates. Use bank statements and accounting records for exact totals.

Third — do not net transactions. If you paid the LLC $10,000 and the LLC paid you $3,000, report each direction separately on the appropriate lines. Do not enter $7,000 as a net figure.

Parts V, VI, and VII — Special Transactions

These three sections cover non-monetary transactions, cost-sharing arrangements, and partnership-related transactions. The vast majority of small foreign-owned LLCs leave all three parts completely blank. They are designed for multinational corporations with complex inter-company structures.

If you have a simple single-member LLC with only cash transactions, skip these parts entirely.

Part VIII — Additional Information

Part VIII contains yes/no questions about the nature of your transactions and recordkeeping. Most small foreign-owned LLCs answer No to everything here.

Line 40 — Did the reporting corporation fail to maintain records: Answer No. If you did not keep records, consult a CPA before filing.

Line 41 — Is the foreign related party a foreign government: Almost always No for individual owners or private companies.

Line 42 — Treaty-related transactions: Answer No unless a CPA advises otherwise.

If you answered Yes to any question, attach a detailed written explanation.

Part IX — Signature and Submission

Signature line: The foreign owner or authorized officer signs under penalty of perjury, certifying all information is true and complete.

Date: Must be on or before the filing deadline.

Title: Enter "Owner" or "Managing Member" for a single-member LLC.

Preparer section: If a CPA prepared the form, they complete this section with their firm name, PTIN, and address.

An unsigned form will be rejected. For fax submissions, a typed signature is acceptable.

How to submit: Foreign-owned single-member LLCs submit by fax to 855-887-7737 (recommended, scan at 300 DPI or higher) or by mail to Internal Revenue Service, 1973 Rulon White Blvd, Ogden, UT 84201 (use certified mail with return receipt). Do not attempt to e-file — the IRS does not accept electronic filing for Form 5472 submitted with a pro forma 1120.

💼 Arik's Corner"Fax. In 2026. I know. The IRS has its reasons. I assume. Regardless — fax is the better option. Mail gets lost at the Ogden processing center more often than anyone at the IRS will admit publicly."— Arik Rozen, CPA

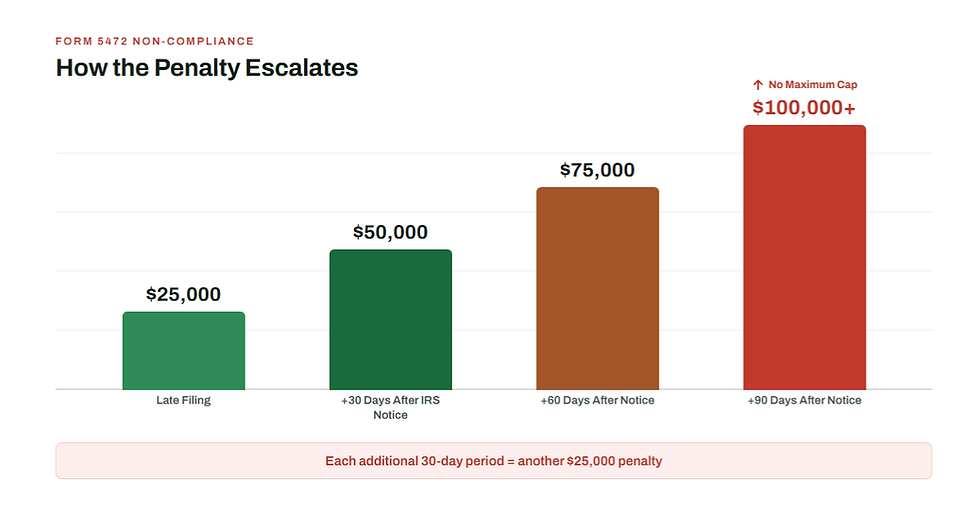

IRS Form 5472 Penalties — What You Risk by Not Filing

The IRS penalty structure for Form 5472 non-compliance is severe, automatic, and has no ceiling. Understanding it fully is the best motivation to file correctly and on time.

The $25,000 Base Penalty

The IRS assesses a $25,000 penalty for each Form 5472 that is:

Filed late (even one day after the deadline)

Filed incomplete (missing required information)

Not filed at all

This penalty is automatic. It is generated by IRS systems when a return is processed — no human review, no warning notice, no grace period.

Continuing Failure Penalties

If the IRS sends you a notice of delinquency and you fail to respond within 90 days, an additional $25,000 penalty is assessed for each 30-day period (or fraction of a period) that the failure continues.

There is no maximum limit on this continuing penalty.

Example: You miss the April 15 deadline. The IRS sends a notice in August. You do not respond. After 90 days, you face:

Original penalty: $25,000

First 30-day period: $25,000

Second 30-day period: $25,000

Third 30-day period: $25,000

Total exposure: $100,000 — from a single unfiled form.

Multi-Year Non-Compliance — How Penalties Stack

The $25,000 penalty applies per form, per year. If you missed filing for multiple years:

2 years missed = $50,000 base penalty exposure

3 years missed = $75,000 base penalty exposure

3 years missed + continuing failure = potentially $150,000+

This is not a hypothetical scenario. Our CPA team handles multi-year penalty resolution cases regularly. The founders who face the largest penalties are almost always those who delayed action after discovering the issue.

Statute of Limitations Stays Open Indefinitely

Normally, the IRS has three years from the date of filing to audit a return and assess additional taxes. When Form 5472 is not filed, this three-year clock never starts. The IRS can audit the entire tax return for that year at any point in the future — years or even decades later — with no statute of limitations protection.

Criminal Penalties for Willful Failure

In cases of intentional failure to file or fraudulent submissions, criminal penalties including fines and imprisonment may apply. These cases are rare but real, and they underscore why compliance is not optional.

💼 Arik's Corner: "$25,000 penalty for not filing a form. The IRS calls this 'non-compliance.' We call it very motivating."— Arik Rozen, CPA

How to Fix a Missed Form 5472 Deadline

Discovering you missed a Form 5472 filing deadline is stressful — but it is fixable. The key is acting immediately and strategically. Here is the exact protocol our CPA team follows for late-filing clients.

Step 1 — Do Not File Late Without a Defense Strategy

Many founders' first instinct is to quickly mail in a late form to "get it done." This is a critical mistake.

When a late Form 5472 arrives at the IRS, automated systems immediately generate a $25,000 penalty notice before any human reviews your case. Filing without a professional Reasonable Cause statement attached means almost certain penalty assessment.

Step 2 — Prepare Your Reasonable Cause Abatement Application

The IRS allows penalty relief under two main pathways:

Reasonable Cause Abatement: If you can demonstrate that you exercised ordinary business care but were unable to comply due to circumstances beyond your control — such as relying on incorrect professional advice, serious illness, lack of awareness of a newly applicable requirement, or inability to access records — the IRS may waive the penalty in full.

First-Time Abatement: If you have a clean prior compliance history (no penalties in the preceding three years), you may qualify for automatic administrative relief under the First-Time Abatement program.

A professionally drafted Reasonable Cause statement, prepared and signed by a licensed CPA, significantly increases the success rate of penalty removal requests.

Step 3 — File All Missing Years Simultaneously

If you missed more than one year, all delinquent returns must be prepared and submitted together as a coordinated package. Filing them separately at different times reduces your abatement success rate and creates gaps in your compliance record that the IRS will scrutinize.

Step 4 — Stop the Continuing Penalty Clock Immediately

If you have already received an IRS notice of delinquency, the 90-day clock before continuing penalties begin is already running. Filing the late return — even without a finalized abatement application — stops the continuing penalty clock. Do not wait for the abatement to be approved before submitting the late forms.

💼 Arik's Corner: "Mistake #11: Googling 'do I need to file Form 5472' in April. You do. You always did."— Arik Rozen, CPA

10 Common Form 5472 Mistakes to Avoid

After 22 years and 230,000+ filings, our CPA team has seen every possible error a foreign-owned U.S. company can make on Form 5472. Here are the ten most common — and how to avoid each one.

Mistake 1 — Failing to Report All Reportable Transactions

The error: Reporting only the transactions you remember, or only the ones that involved large amounts of money, while omitting smaller transfers, accruals, or non-cash exchanges.

How to avoid it: Maintain a running transaction log throughout the year and reconcile it against your bank statements and accounting records before filing. Every transfer between you and your U.S. company counts — regardless of size.

Mistake 2 — Misclassifying the Related Party Relationship

The error: Incorrectly describing how the related party is connected to your U.S. company — for example, reporting a foreign sister company as a direct shareholder when both are owned by the same parent.

How to avoid it: Create and maintain a clear organizational chart showing all entities and their ownership percentages. Review it before each annual filing.

Mistake 3 — Using Inconsistent Currency Exchange Rates

The error: Converting some transactions at the spot rate on the transaction date and others at the annual average rate, creating internal inconsistencies the IRS flags immediately.

How to avoid it: Choose one IRS-approved conversion method — typically the annual average exchange rate — and apply it consistently to all transactions reported on the form.

Mistake 4 — Leaving Sections Blank or Using Estimates

The error: Leaving required fields empty because the exact figure wasn't immediately available, or filling in rough estimates instead of confirmed amounts.

How to avoid it: If an exact figure is unavailable at filing time, note this on the form with your best estimate and file an amended return once accurate records are confirmed. A good-faith attempt is always better than a blank field.

Mistake 5 — Filing Form 5472 Without the Pro Forma 1120

The error: Foreign-owned single-member LLC owners submitting Form 5472 as a standalone document, without attaching it to a pro forma Form 1120.

How to avoid it: The IRS will reject a standalone Form 5472 from a single-member LLC. The two forms must be prepared and submitted as a single package. If you are unsure how to prepare the pro forma 1120, work with a licensed CPA.

Mistake 6 — Filing One Form for Multiple Related Parties

The error: Combining all related-party transactions onto a single Form 5472 when transactions occurred with multiple different related parties.

How to avoid it: A separate Form 5472 must be filed for each related party with whom reportable transactions occurred. If you had transactions with three related parties, you need three separate forms — all due by the same deadline.

Mistake 7 — Reporting Different Amounts on Form 5472 and Other Returns

The error: Reporting $1 million in purchases from your foreign parent on Form 5472 but showing $1.2 million on your income statement or other tax forms.

How to avoid it: Reconcile Form 5472 against all other tax forms and financial statements before submission. Any discrepancy triggers IRS scrutiny. Investigate and document every difference before filing.

Mistake 8 — Ignoring Non-Monetary Transactions

The error: Assuming Form 5472 only applies to cash transactions and therefore not reporting services, property use rights, or intellectual property provided by a related party without payment.

How to avoid it: Non-monetary transactions — including free services, license-free use of IP, and below-market arrangements — are all reportable on Form 5472 Section 5. Track and disclose them all.

Mistake 9 — Misreporting Loan Balances and Interest Payments

The error: Reporting only the interest paid on a related-party loan without disclosing the outstanding loan principal balance.

How to avoid it: Both the loan balance and each interest payment must be reported separately. Maintain detailed loan records including principal amounts, interest rates, payment schedules, and any changes to loan terms.

Mistake 10 — Missing Mid-Year Changes in Foreign Ownership

The error: Filing based on the ownership structure at year-end and failing to disclose a change in foreign ownership that occurred mid-year — for example, a new foreign investor acquiring a 25% stake in July.

How to avoid it: Ownership changes that occur at any point during the tax year must be reflected in the filing. Review ownership structure quarterly and document any changes as they happen.

💼 Arik's Corner: "Can I file Form 5472 myself? Technically yes. You can also technically cut your own hair. Results may vary."— Arik Rozen, CPA

Frequently Asked Questions About IRS Form 5472

Can Form 5472 be e-filed?

Yes. Form 5472 can be e-filed, and the IRS strongly encourages electronic submission. E-filing is faster, more secure, and generates a confirmation receipt upon acceptance. The form must be submitted through an IRS Authorized e-File Provider as part of the corporate return package — it cannot be e-filed as a standalone document. Form5472.online is a verified IRS Authorized e-File Provider.

Do I need to file Form 5472 if my LLC had no transactions this year?

If your foreign-owned single-member LLC had absolutely no reportable transactions during the tax year — meaning no capital contributions, no distributions, no formation costs, no maintenance fees, and no financial activity of any kind — you may not be required to file Form 5472 for that year.

However, as described in the Zero-Income Trap section above, a truly transaction-free year is exceptionally rare. If any money moved between you and the company at any point during the year, a reportable transaction occurred and the filing requirement applies. When in doubt, consult a licensed CPA.

What if I made a mistake on a previously filed Form 5472?

If you discover an error after filing, you must submit an amended return as quickly as possible. The process:

Prepare a corrected Form 5472

File an amended corporate return (Form 1120-X for corporations)

Attach the corrected Form 5472 to the amended return

Include a written statement explaining the specific changes made and why

Filing an amendment promptly can reduce potential penalties related to the original error.

How does Form 5472 relate to Form 1120?

For foreign-owned single-member LLCs and C-Corporations, Form 5472 is never submitted alone. It is always attached to and filed together with Form 1120 (or a pro forma Form 1120 for LLCs). The Form 1120 serves as the parent return; Form 5472 is the attached disclosure schedule. Both must be complete and accurate for the filing to be accepted by the IRS.

What records should I keep to support my Form 5472 filing?

Retain the following records for a minimum of seven years from the filing date:

Corporate formation and ownership documents

Financial statements for the tax year

Invoices and receipts for all related-party transactions

Bank statements showing all transfers between the foreign owner and the U.S. entity

Loan agreements and interest payment records

Service contracts with related parties

Transfer pricing documentation (for C-Corporations)

Currency exchange rate records used for conversions

All correspondence with the IRS related to Form 5472

Because the statute of limitations for an unfiled Form 5472 never closes, strong permanent record-keeping is your best protection against future IRS inquiries.

How long does it take to file Form 5472?

When prepared by our licensed CPA team, standard turnaround for Form 5472 and pro forma Form 1120 is 10 business days from the date you complete your information questionnaire. Expedited 3-day service is also available.

Do I need a CPA to file Form 5472, or can I do it myself?

There is no legal requirement to use a CPA. However, given the $25,000 automatic penalty for errors, the pro forma 1120 requirement, the complexity of transaction categorization, and the IRS's zero-tolerance enforcement posture on this form, professional preparation is strongly recommended.

A licensed CPA does not just prepare the form — they provide professional accountability, reduce audit risk, and can represent you before the IRS if questions arise. The cost of professional preparation is a fraction of one year's penalty.

💼 Arik's Corner: "Somewhere right now, a foreign founder is reading this at 11pm wondering if they need to file Form 5472. They do. Also: hi. We can help."— Arik Rozen, CPA

Ready to File? Let Our CPA Team Handle Everything.

Form5472.online is part of TAXUSA GROUP — a licensed CPA firm with 230,000+ filings completed since 2004. We are a verified IRS Authorized e-File Provider, and every filing is prepared and signed by a licensed CPA with an IRS-issued PTIN.

Our Zero Penalty Guarantee means that if you receive a penalty notice due to an error in our filing, we represent you directly with the IRS until the issue is fully resolved — at no additional cost.

✓ 230,000+ Filings Completed✓ Licensed CPA — Virginia #025991✓ IRS Authorized e-File Provider✓ Zero Penalty Guarantee✓ 10-Day Standard Turnaround

Questions? Email us at file@form5472.online or start a chat with our team.

About the Author: Arik Rozen is a U.S. Certified Public Accountant licensed by the Commonwealth of Virginia (License #025991) since 2001. He serves as Head of Tax Filing at form5472.online and has overseen tens of thousands of international tax filings over 22 years of practice. He specializes in IRS compliance for foreign-owned U.S. LLCs and corporations.

This article is for informational purposes only and does not constitute legal or tax advice. Filing requirements vary by individual situation. Consult a licensed tax professional for advice specific to your circumstances.

Disclaimer — Not Legal or Tax Advice

This guide is provided for general informational and educational purposes only. It does not constitute legal advice, tax advice, accounting advice, or any other professional advice, and does not establish a client–professional relationship of any kind.

The information on this page is based on IRS publications and instructions as of the 2024/2025 tax year. Tax laws, regulations, penalties, and filing requirements change frequently. We make no representations or warranties — express or implied — that the information is current, complete, or accurate for your specific situation.

Your tax situation is unique. Factors such as your country of residence, treaty status, type of business activity, transaction types, and ownership structure can significantly affect your filing obligations. What applies to one taxpayer may not apply to another.

Always consult a licensed CPA, tax attorney, or enrolled agent who is familiar with international tax law and IRS compliance requirements before filing any IRS form, making any tax decision, or relying on this guide for your specific circumstances.

Form5472.ai and its operators are not liable for any errors, omissions, losses, penalties, interest, or damages of any kind arising from your use of or reliance on this guide. Use of this guide is at your own risk.

IRS Circular 230 Notice: To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained on this website is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code, or (ii) promoting, marketing, or recommending to another party any transaction or matter addressed herein.

Comments